And going forward, how will this unfold in the next economic cycle?

As a specialist VC, researching this note has been a fascinating excuse for a thought experiment or two. To start, let’s explore how to define what constitutes a specialist vs generalist.

Some industry analysts mark a specialist VC as someone who focuses on just one sector. I have a slightly different definition, which I’ll come back to later. For now, let’s take a look at the data.

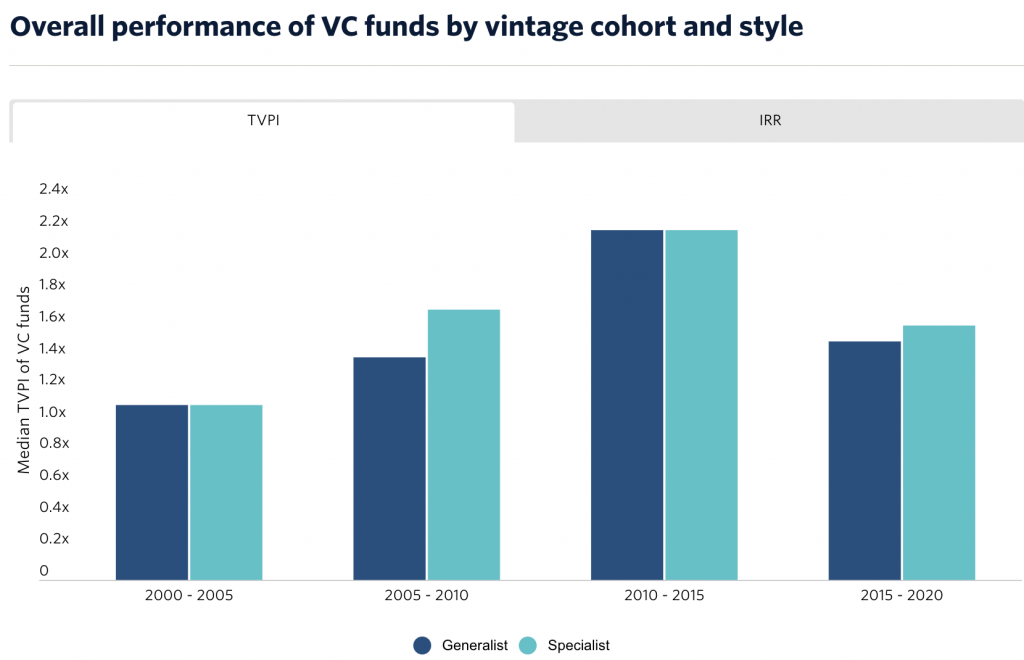

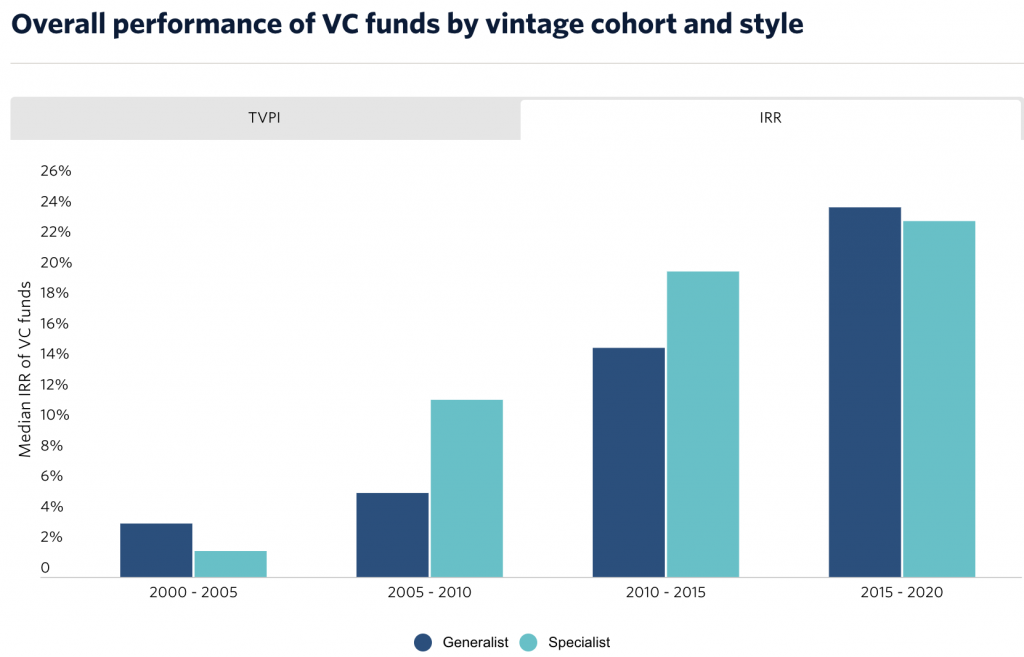

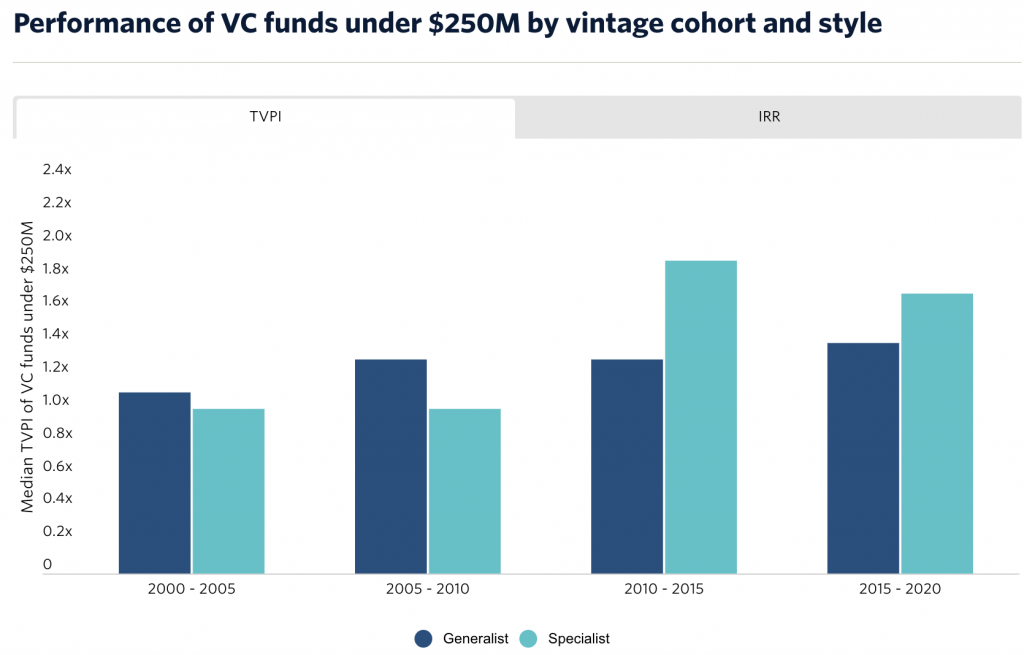

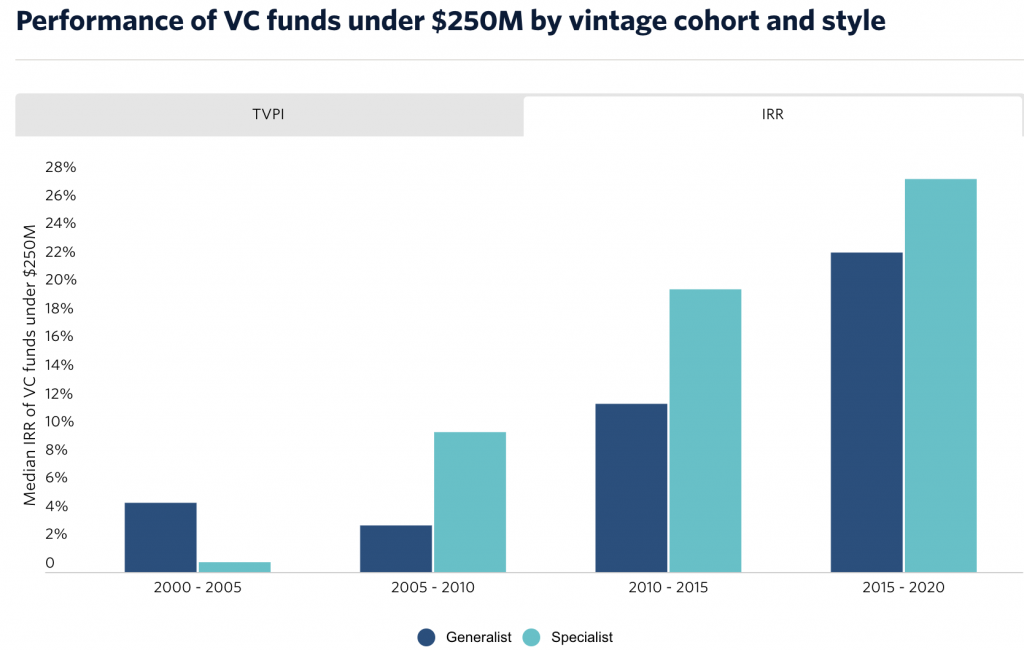

According to Pitchbook, which looked at 1824 VCs over the last 20 years, it turns out that sector-specific VCs outperform (generally, looking at median TVPI or IRR).

Not by a huge margin until you look at smaller funds (sub $250m), where the specialist performance uplift is more impressive.

It’s hard to accurately unpack the data by stage, territory, or in context against inertia and the changing macro backdrop, but we can draw some conclusions.

Generalists seem to do well in good times through diversification, mainly at the later stages. As the specialists miss out on flash trends and in some cases take longer to return capital (especially those in deep tech).

Smaller funds tend to operate at the earlier stages where they can outperform by specialising in a niche, enabling them to focus, and attract ‘more of the same’ outstanding teams.

Horses and courses.

To sate my own thought experiments I wanted to look beyond sector specialists, and broad stage. What about Europe vs US? Earlier stages? VC platform vs no VC platform? Strategies and objectives?

Crystal balling the next decade.

This next economic cycle is going to be a fascinating one for the startup ecosystem with many counterfactuals duking it out. As the West decouples from the East amid war, with silicon tussles for protection, control and production – AI is enabling more software development power, more quickly. According to Scott Guthrie from Microsoft, 40% of code uploaded to Github in March was purely AI generated.

Investors who initially retracted with a nosebleed from recent VC excesses are now piling back into secondaries at a significant discount. Hot sectors such as web3, crypto and the metaverse are firmly back in their boxes while AI keeps the crazy lights on with outsized valuations and raise sizes.

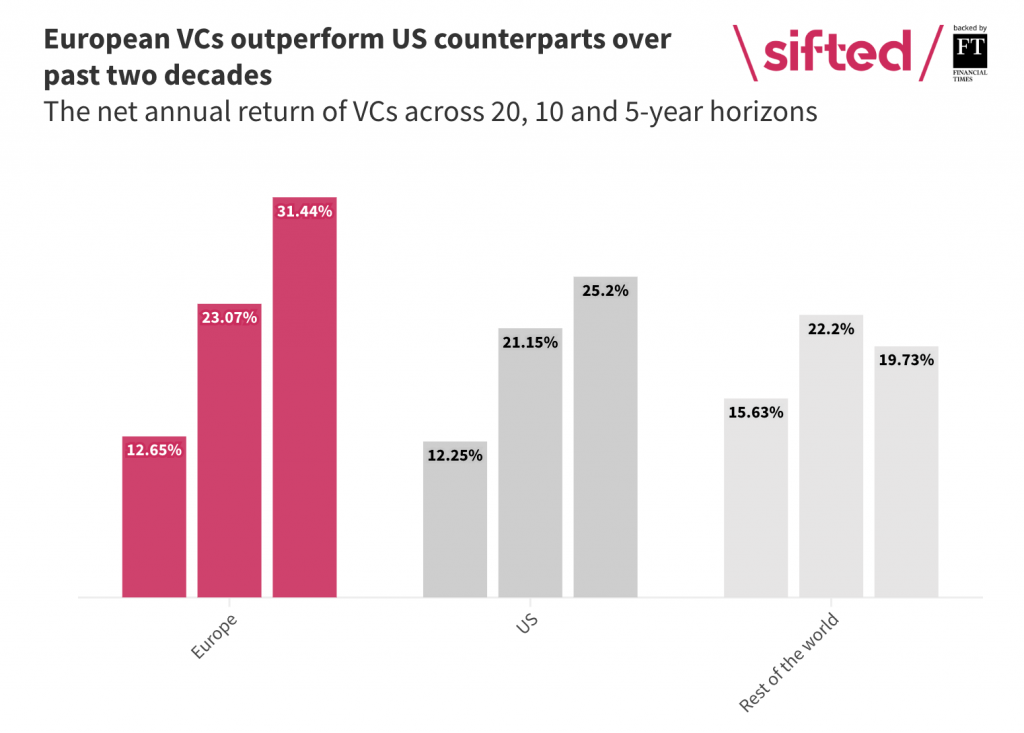

Venture activity perceived as hot in the States over the last 10 years was actually hotter in Europe, according to a new Sifted report.

The surprising state of European venture.

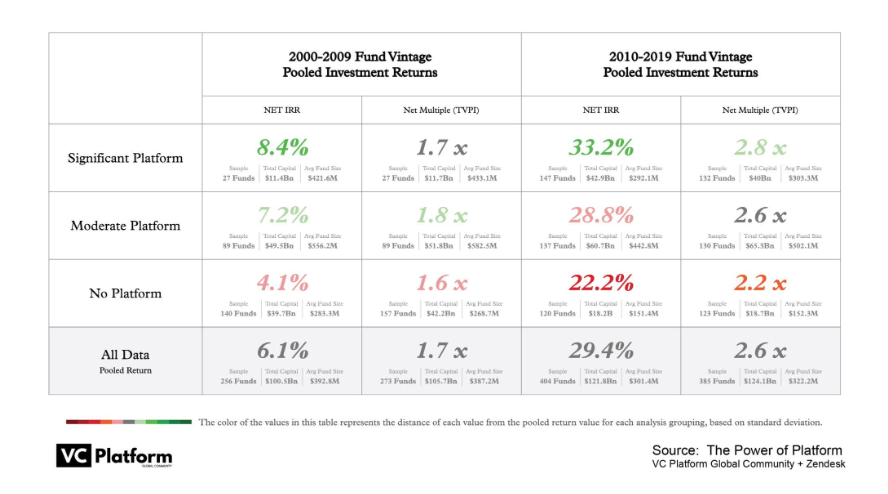

What about platform VC?

Cory Bolotsky and Dale Chang looked at 850 VCs over the last 20 years to ask the question – does platform venture capital (investors who actively support their teams) perform better than those who do little beyond the cash.

You can intellectually answer the question both ways but the data shows that those who more actively support teams in the earlier stages perform better. Anecdotally I can add that the founders who constantly reach out and ask questions are doing better in our portfolio than those who don’t (not just from us or other investors, but via board, advisory and other smart networks).

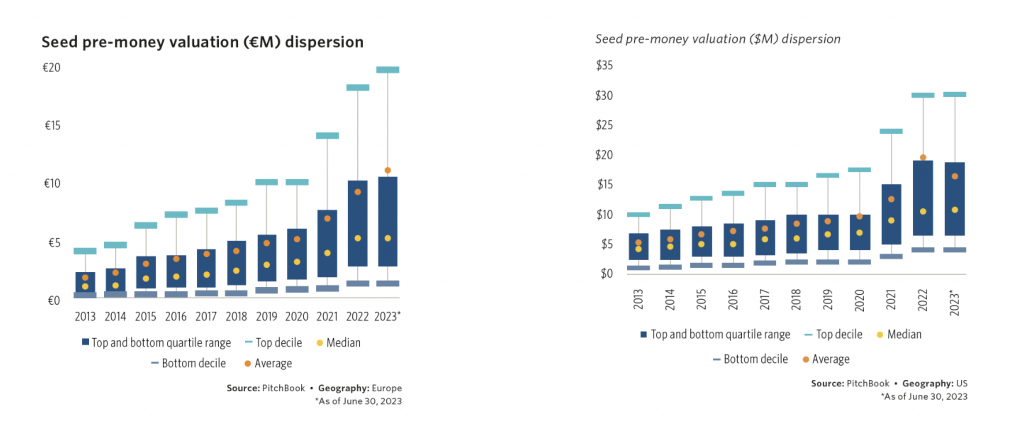

Euro discounts.

In our small corner of the world at seed, in Europe, all of this is being accomplished at a 40% discount. European startups (graph on the left) are still significantly cheaper than across the pond (right).

Looking deeper at more data I’m going to challenge the terminology and put us, and those like us, back in the Specialist box. We don’t focus on one sector but we do focus on big business optimisation (or resource efficiency, depending on which side of the seesaw you’re sitting). And we do focus at seed, using a platform approach, to serve technical teams solving enterprise scale problems. Pretty specialised in my books! And benefitting from all of the same upsides as the sector specialists.

So how will this play out for the next decade?

There is nothing to suggest that the next ‘good times’ is anywhere close (but boom and bust *will* consistently rotate because, humans). It looks like we’ll generally see a protracted period of low economic growth for most (read ‘opportunity for startups’). Sure IPOs will creep back, more trade sales will consolidate sectors to gain competitive advantage, as those without solid units will close their doors.

Looking forwards we still have fundamental challenges to face that will absolutely need fundamentals startups to innovate and fuel our future. Those focusing on climate, manufacturing, efficiency, agriculture, energy, water, supply chains etc will continue to do well – as all businesses become AI businesses. Against a backdrop of sluggish markets, high(er) interest rates, and no more free money.

All of which suggests a specialised approach will win, however we choose to define that, and maybe now is a great excuse for new kinds of definable VC specialists? Perhaps even one that looks beyond financial returns for our new world.