This is not investment advice.

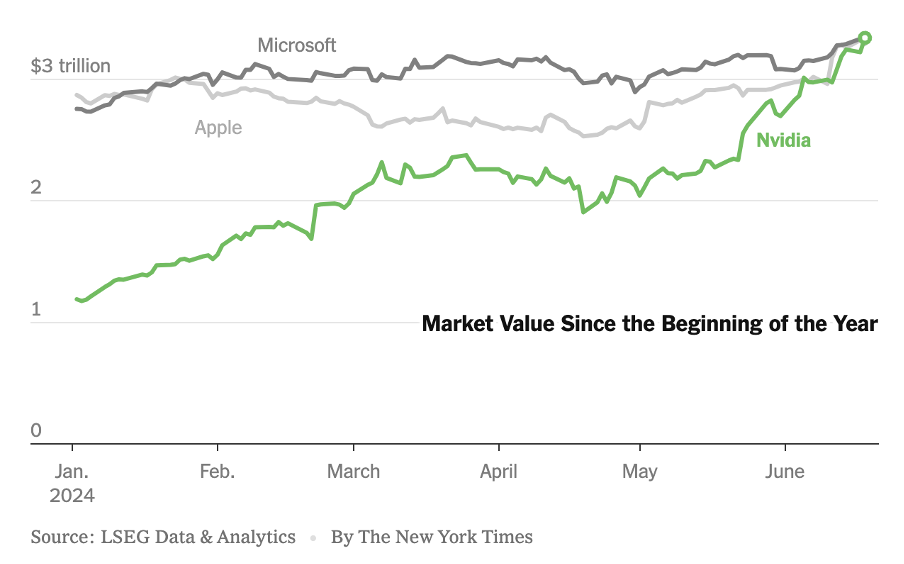

Nvidia Continues to Crush It

Despite a wobble in April, markets had a strong run in Q2. The S&P500 clocked up a 3.9% gain, and the Nasdaq-100 performed even stronger, with a 7.8% growth in the same period.

Once again, tech was in the driving seat, with Google (up 20.5%), Apple (up 22.8%), and Nvidia (up 36.7%) driving stellar growth.

I wrote earlier in the year that I thought Nvidia looked reasonably fully valued at $2.2trn. In late June, the company burst through a $3trn, as it continues to defy gravity. This briefly made the company the most valuable in the world. It also made Nvidia worth more than all of the FTSE100 or CAC40.

How does one get to $3trn?

The question is – how can a company with revenue just north of $100bn be worth more than $3trn? And be worth roughly the same as Apple – a company with more than $350bn in annualised revenue?

The answer is twofold: profitability and growth. Because, while Apple (a formidable company) has a net profit margin of 26% and Microsoft (an also formidable company) has a net profit margin of 35%, Nvidia clocks up an incredible 57%. And that is while growing revenue more than 260% year-over-year.

Never before has a company grown so fast at this scale while being also being so profitable. So while 52-times earnings look like a slightly cooky multiple, Nvidia just keeps blowing the doors off everyone’s expectations.

Comparing the Pros and the Cons

Let’s look at the case for and against:

Bring out the bulls

- It’s all about AI. Every board of every Fortune 500 company is panicking that they’ll be left behind in the AI race. Every tech investment gets scrutinised, and every possible $ is being directed towards AI initiatives. Not even the internet was such a perfect storm. And so far, Nvidia has been the main beneficiary of this investment as everyone races to train AI models.

- Product superiority. Not only does Nvidia have the best chips for AI, the company also has CUDA – the software framework used by AI researchers to train models. As the industry has standardised on CUDA for AI model development, Nvidia has lock-in through the whole stack. This makes them hard to dislodge.

- Unrivalled financial performance. As outlined above. No company has ever delivered this mixture of growth, scale and profitability before. And points 1 and 2 above suggest that the good times could continue. Cue investor excitement.

Line up the bears

- Growth already fully priced in? You can currently buy the S&P500 at 28 times earnings. 52 times earnings look expensive in comparison, even with the expected growth potential.

- Is a lot of Nvidia’s revenue experimental? The headline is that enterprise customers have spent close to $100bn buying chips for their AI experiments. How much revenue growth or cost savings has this investment created for those companies? And if the benefit hasn’t matrialised yet, what are the odds that the chip spend will keep growing?

- Competitive threats. No company has ever sustained a 57% net margin at this scale, let alone for a prolonged period. Dozens of companies have raised billions to go after the AI chip market opportunity. Even if the AI chip segment continues to grow, a) can Nvidia keep capturing so much of the market, and b) can they possibly keep their profit margins so high, given more competition?

As I wrote back at the start of the year – one thing is for sure: Human psychology wants to lean into trends. No matter which side of the above arguments you come down on, there are good momentum-related arguments for the continued growth in Nvidia’s share price. We know that nothing keeps growing forever. But, in Q2, investors continue placing bets that the future road for Nvidia is pointing up and to the right.

As a final note, the company announced recently that several of NVIDIA’s directors have been booking profit by selling some of their shares:

Jensen Huang still owns shares worth more than $100bn, so selling $100m worth of shares does not look alarming in the overall context. But still, worth noting.

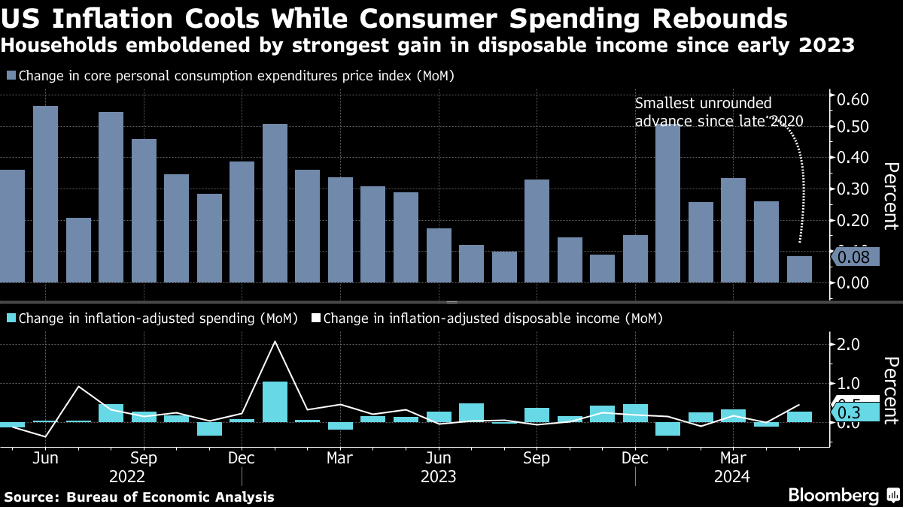

What else is happening in markets?

All the real excitement is about AI, tech transformation, and growth—and rightly so. But the yin and yang of interest rates and inflation are still powerful undercurrents that shape our markets. Bloomberg reported that the “core personal consumption expenditures price index” decreased to less than 0.1% in May. This index is the Federal Reserve’s preferred measure of inflation, as it strips out volatile food and energy prices.

As the May reading was the smallest advance since 2020, there is optimism that we now. Finally. Can. Inch. Our. Way. Towards US interest rate cuts. With all the associated boosts to the real economy.

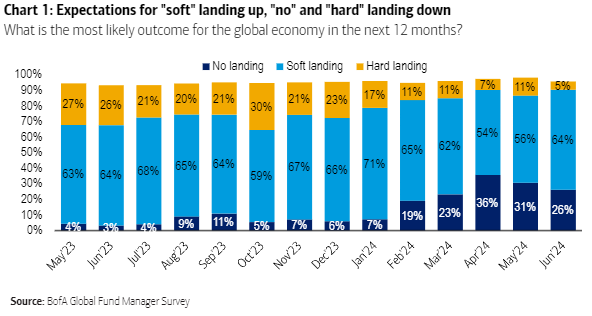

At this part of the business cycle, growth typically slows down, and the economy enters a spell of recession before rebounding back to growth. Over the past two years, the economics discussion has been about whether the US would get to a hard or a soft landing. I.e., would the economy crash or “just” get to a mild recession before the resumption of normal service.

What Type of Landing Ahead?

Although US inflation has been stubborn, growth has continued at a reasonable pace. This year, the discussion has started to shift to a point where more than a quarter of global fund managers think there might be no “landing” at all (according to Bank of America). This is remarkable. Bond markets have warned of an upcoming recession for a long time (through the inverted yield curve). It would be the first time we've had such strong signals with no recession in the end.

The odds still look like a “soft landing”. But it’s remarkable if the US economy can keep growing—especially in the context of geopolitical upheaval and US political uncertainty.